![]()

![]()

![]()

![]()

RI Coastal Resources Management Council

...to preserve, protect, develop, and restore coastal resources for all Rhode Islanders

![]()

![]()

![]()

![]()

...to preserve, protect, develop, and restore coastal resources for all Rhode Islanders

Whitehouse, Fugate educate real estate appraisal industry on impacts of SLR, CC

July 10, 2017, PROVIDENCE – Rhode Island will be particularly susceptible to the impacts of climate change and sea level rise by 2100, and one of the industries to feel those impacts acutely is the real estate and appraisal industry, according to experts who recently spoke to members of the Massachusetts and Rhode Island Chapter of the Appraisal Institute.

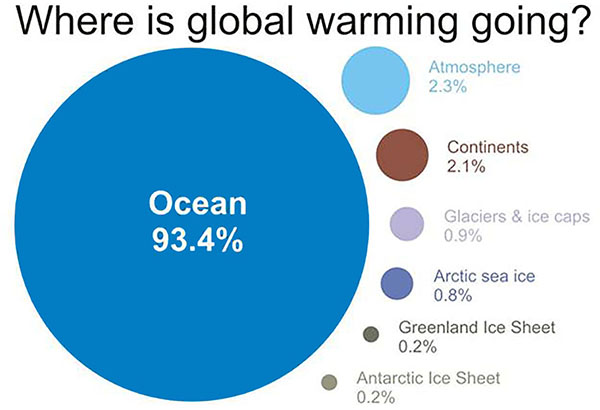

"The ocean absorbs most of the excess heat generated by greenhouse gases” – 93.4 percent, said Senator Sheldon Whitehouse (D-RI). “It’s the earth’s heat regulator.” And as a direct result of all of that heat absorption, said the Rhode Island senator, the oceans are warming.

“A three or four-degree change in water temperature wouldn’t make much of a difference to you and me, but for life in our oceans, it’s what [scientists] call an ecosystem change,” he told a room full of real estate appraisal professionals on June 26 at Save The Bay. The talk given by Whitehouse, along with Grover Fugate, executive director of the R.I. Coastal Resources Management Council (CRMC), Teresa Crean of the University of Rhode Island’s Coastal Resources Center and R.I. Sea Grant, and Marc Guerin of Citizens Financial is part of a series targeting Rhode Island industries and organizations to educate them on the impending impacts of rising seas and climate change in the Ocean State.

The CRMC, the state’s coastal management and permitting agency, is unique, according to Fugate – unlike other coastal states, it is a direct-permitting agency, making the same land-use decisions as municipalities, but with a professional staff of engineers, biologists, and policy analysts that cities and towns do not typically possess.

“We will never stop people from building on the shore, but they should understand their risk,” Fugate said. The R.I. Shoreline Change Special Area Management Plan (Beach SAMP), currently being developed by the CRMC, URI CRC and R.I. Sea Grant with other partners, aims to do just that. Part of the ongoing effort includes Climate 101 training for municipalities, developed by URI and coming to all 21 coastal communities soon, according to Crean.

In addition to understanding the implications of sea level rise, Fugate said the industry also needs to be prepared for increased severe storm activity and erosion, and what that means for Rhode Island real estate. A 2013 Federal Emergency Management Agency (FEMA) study estimated that high-risk flood hazard zones (or Special Flood Hazard Areas or SFHAs) will increase by 45 percent nationally by 2100, and by 55 percent in coastal areas, assuming no change in shoreline, according to an article on Freddie Mac’s web site: (http://www.freddiemac.com/research/insight/20160426_lifes_a_beach.html).

It is estimated that our erosion rate will double by 2065, and increase by two-and-a-half by 2100, Fugate said. The Matunuck area of South Kingstown currently averages approximately 4 feet of erosion per year. And wind and impacts of sea level rise on ground water are other factors that largely haven’t been taken into account.

Painting by John Russell Bartlett, part of the RI Historical Society Collection. The storm hit New England on September 23, 1815. Water reached 13 feet, 9 inches above mean high tide in downtown Providence on Sept. 21.

Global warming graph – This graphic shows where the increased heat from global warming is being stored on Earth (for the period from 1993 to 2003), taken from the Intergovernmental Panel on Climate Change (IPCC). (Source: Skeptical Science, from IPCC AR4 5.2.2.3)

“Rhode Island has not experienced a major hurricane since 1954 – we don’t have that institutional knowledge and memory anymore,” he said. And the most recent maps developed by FEMA underestimate risk to coastal properties from storm surge, erosion and flooding by reducing the flood elevations and not recognizing the effects of sea level rise during the structures’ lifetime. Through the Beach SAMP, tools are now available to help people anticipate future conditions, and let them build for those future conditions.

“We’ve developed STORMTOOLS and CERI so that we no longer have to wait until a storm hits to see what the damage will be – we can see it before it happens,” Fugate said. Both STORMTOOLS and CERI (Coastal Environmental Risk Index) are GIS-based mapping tools - STORMTOOLS provides coastal flooding, sea level rise, and storm event scenarios; and CERI predicts storm surge and wave action, combined with erosion maps and assigns damage functions to structures – developed under the SAMP to give a more detailed projection of future conditions.

If a structure is in a high-risk flood hazard zone or a SFHA as determined by FEMA, a buyer must get flood insurance in order to get a mortgage. For owners of existing structures within flood zones, taking out a line of credit, obtaining a reverse mortgage, or acquiring any federally-attached loan will require the borrower to purchase flood insurance. For property owners looking to build, any structure built within the Special Flood Hazard Area will require flood insurance if a mortgage is needed, and new construction will have to meet the most recent building codes, according to Beach SAMP web site: http://www.beachsamp.org/relatedprojects/coastalpropertyguide/flood-zones/ . The site also advises that for properties not currently in a FEMA flood zone, checking the 500-year flood zone might assist in determining future risk. “Many lenders assess flood-risk for the life of the loan, and with increasing sea-level rise and shoreline change, the long-term impacts on the property may come into play.”

Most likely, impacts of climate change and sea level rise on the real estate appraisal and associated markets will be felt locally at first, said Brad Hevenor, an appraiser and vice chair of the Rhode Island Chapter of the Appraisal Institute. Superstorm Sandy was a good example of that – there was an immediate market response in some neighborhoods, which suggested that buyers’ preferences for waterfront properties was at least “temporarily rattled,” he said. And there has been an acknowledgment of flood risk among borrowers, even if it’s often only a cash-flow issue with property owners who are unhappy with flood insurance rates or requirements, he added. The largest unknown is what it will take for permanent changes in the market.

“While we have the benefits of convincing data and projections regarding sea level rise, one of the biggest uncertainties is whether economic disruptions will happen gradually, or whether there could be a precipitating event or series of events which causes a more rapid shock to real estate markets,” Hevenor said. “The collapse of real estate markets in 2007-2008 certainly should have taught us how quickly weaknesses in the financial or banking system can become a crisis.”

Hevenor said that was one of the reasons he saw this as an important issue to raise with real estate appraisers, particularly given their position in risk management in the lending and finance industry.

“We hold a position of public trust in providing homeowners, banks, and investors with sound analysis, particularly regarding real estate risks,” he said. “If appraisers are aware of the economic and real estate risks, they could not only be among the first to notice it, but in a unique position to analyze and communicate the economic impact as it happens. That is why it is so important for valuation professionals to become aware of work that is being done to measure and forecast the potential impacts [of climate change and sea level rise].”

According to FEMA, 20-25 percent of flood losses occur at properties outside the Special Flood Hazard Area (SFHA). Floods are also the most common and widespread of all weather-related natural disasters in the United States, according to the National Oceanic and Atmospheric Administration’s National Severe Storms Laboratory.Stedman Government Center

Suite 116, 4808 Tower Hill Road, Wakefield, RI 02879-1900

Voice 401-783-3370 • Fax 401-783-2069 • E-Mail cstaff1@crmc.ri.gov

![]()

![]()

An Official Rhode Island State Website